The Monetary Policy Committee of the Reserve Bank of India conducted its bi-monthly policy meeting from 5th to 7th June 2024. The MPC has decided to keep the policy rates unchanged for the eighth consecutive time. The RBI in its recent policy meeting, announced that the economic conditions are stable and they would be happy with a wait and watch role.

The RBI has decided to keep the stance of withdrawal of accommodation while supporting growth. However, with controlled inflation, strong external sector & forex reserves, and a good growth rate, it can be said that the economy is in a sound position with a growing trajectory. Keeping this in mind, in my opinion, the RBI may think of interest rate cuts in the future, rather it has started preparing for interest cuts. There are clear pieces of evidence discussed below that will validate the statement.

Evidences of Possible Rate Cuts and Change in Stance by RBI

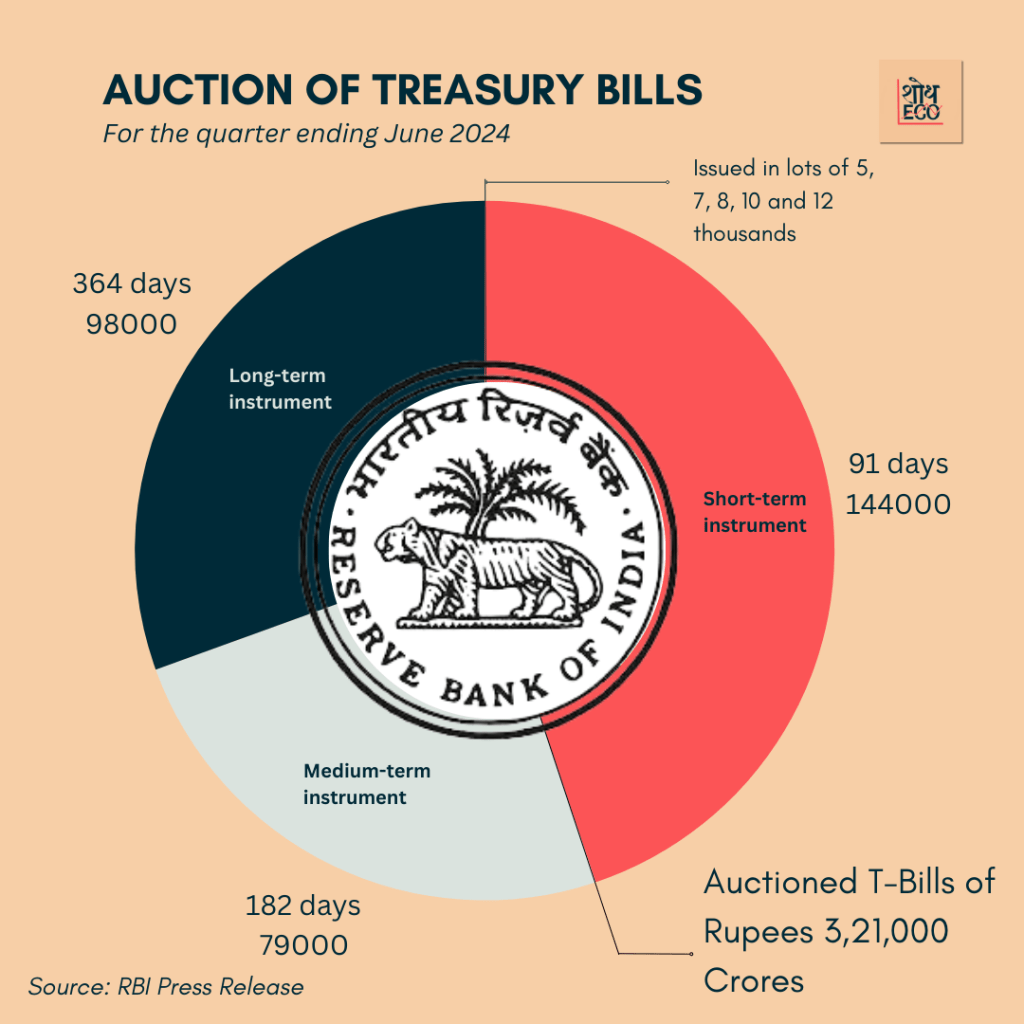

- Treasury Bill Auctions

The RBI notified the treasury bill auctions on March 27 for 91 Day, 182 Day, and 364 Day Treasury Bills. The particulars are as follows:

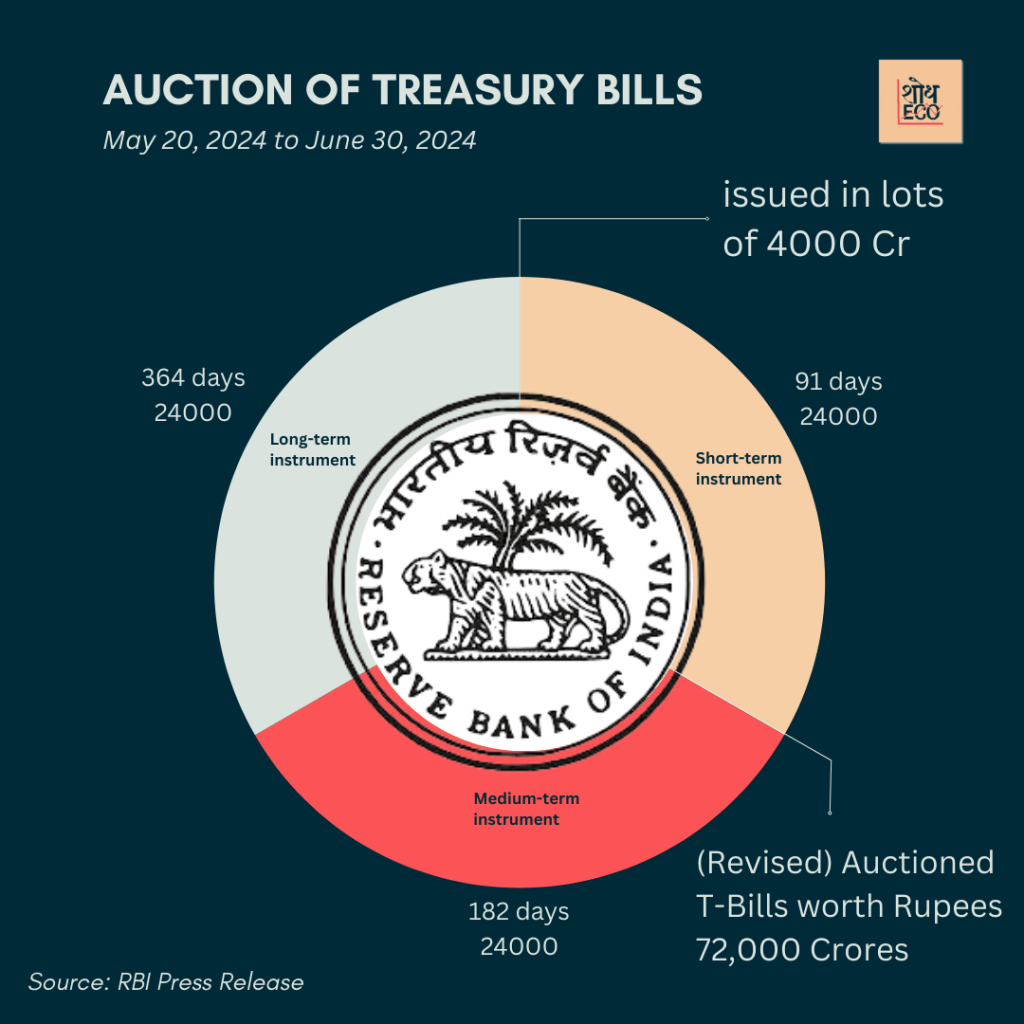

However, on May 22, it revised the T Bill auction amounts. These are as follows:

This action of RBI can be interpreted in two ways. Firstly, revising the T Bill auction amounts indicates that RBI will also have to repay the T Bills maturing on May 22, 2024. Secondly, the revised amount of the T Bills is significantly less than the previous amounts. Thus, here it is safe to say that, RBI is injecting liquidity through the repayment of maturing T Bills, and through the reduction in T Bills as auction amounts absorb less liquidity. Hence, the RBI is looking to keep high liquidity in the market. This can be considered as one of the signs of possible rate cuts in the next quarter.

- Buy Back of Dated Government Securities

The RBI has announced buyback of government securities thrice in the month of May for the amounts of 40,000/- Cr, 60,000/- Cr, and 40,000/- Cr, respectively. All these securities are maturing in FY2024 and FY2025. Buyback of dated government securities before the maturity indicates that the central bank has greater short-term liquidity and thus is focusing on repaying the liabilities maturing in Q3 & Q4 of FY2024 and FY2025 well before the term. Thus, this will again lead to an increase in the money supply. Another point to focus is that banks generally demand lower yields on the buyback of securities, hence the falling yields of the long-term securities can be considered as evidence that higher liquidity is being injected into the economy.

- Variable Repo Rate Auctions

The RBI conducts repo and reverse repo auctions to manage the liquidity in the economy. Since the last policy meeting in April 2024, the RBI has only conducted multiple Variable Repo Rate Auctions (VARR).

This indicates that the RBI is catering to the needs of the banks and is ready to inject liquidity into the system as and when required. This also suggests that the RBI has plenteous liquidity with itself. Thus, it may shift its stance to neutral and go for rate cuts in the next MPC meeting.

- Yield Curve Analysis

Following are the currently prevailing rates of different financial instruments:

These rates have been moving closely to each other, and thus, the yield curve has been relatively flatter for the past 3-4 months. A flatter yield curve indicates the short-term and long-term yields do not have much difference. Thus, there are expectations of rate cuts in the future as the yield curve is flatter before the transition. Another point to back this theory is that the RBI has kept the policy rates constant for 8 consecutive times. So it can be predicted that, if RBI is comfortable with the inflation, it may go for a rate cut and stance change in Q3 of FY 2024-25.

Implications of Probable Rate Cuts

- The Long-term yields have already been on the fall since the start of FY 2024-25. As the rate cuts are done, short-term yields are likely to come down quickly in the G-SEC market.

- Regarding the deposit rates, the less risky deposits may see a slow fall in the interest rates. However, the rates of risky deposits may fall in less time.

- The loans and advances may too see an interest rate fall but, it would be at a slower rate. In Particular, the housing loans may get a little cheaper.

- Largely, the liquidity in the market will increase, which may have an impact on the demand-pull inflation.

Conclusion

Despite the predictions of rate cuts, RBI will still be watchful of the union budget to be presented in the month of July, Fed Reserve actions, the changing dynamics of food inflation, and geopolitical tensions before taking any decision on the change in stance and rate cuts. Thus, despite robust fundamentals of the economy and the hidden actions of RBI towards the interest rate cuts, the MPC will move cautiously before actually implementing the rate cuts, although it is very likely to change its stance from accommodative to neutral in the next policy meeting.